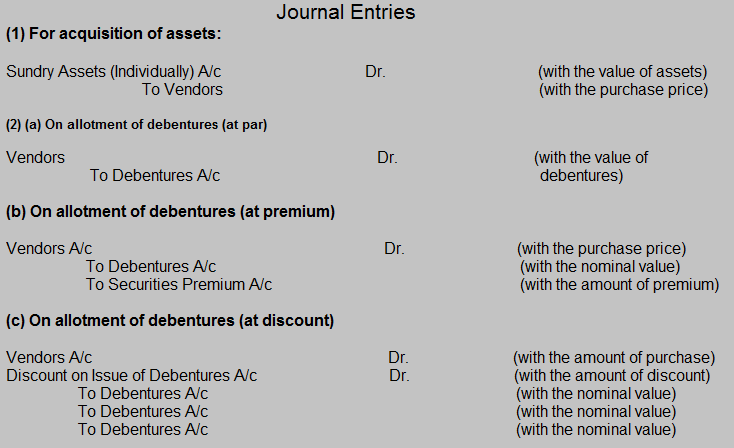

DEBENTURES ISSUED FOR CONSIDERATION OTHER THAN CASH :

The company may allot debentures to the vendors for acquiring some assets as payment for purchase consideration. This issue of debentures to vendors is known as issue of debentures for consideration other than cash.

Notes:

(i) If the value of debentures allotted is more than the agreed purchase price, the difference is debited to Goodwill Account.

(ii) Similarly, if the value of debentures allotted is less than the agreed purchase price, credited to Capital Reserve Account.

Illustration :

Optimist Ltd. purchased building worth Rs.1,20,000 and plant and machinery worth Rs. 1,00,000 from Depressed Ltd. for an agreed purchase consideration of Rs. 2,00,000 to be satisfied by the issue of 2,000, 12% Debentures of Rs. 100 each. Show the necessary journal entries in the books of Optimist Ltd.

Solution:

Journal

| Particulars | Dr.(Rs.) | Cr.(Rs.) |

| Building A/c Dr. | 1,20,000 | |

| Plant and Machinery A/c Dr. | 1,00,000 | |

| To Depressed Ltd. | 2,00,000 | |

| To Capital Reserve A/c | 20,000 | |

| (Purchase of sundry assets and transfer of capital profits as per agreement with the vendor dated…) | ||

| Depressed Ltd. Dr. | 2,00,000 | |

| To 12% Debentures A/c | 2,00,000 | |

| (Being 2,000, 12% Debentures of Rs. 100 each allotted to vendors for consideration other than cash as per Board’s resolution dated…) |