Declaration of dividend (Section 123 of the Companies Act, 2013) :

Section 123 of the Companies Act, 2013 came into force from 1st April, 2014 which provides for declaration of dividend. According to this section:

(i) Dividend shall be declared or paid by a company for any financial year only —

(a) out of the profits of the company for that year arrived at after providing for depreciation in accordance with the provisions of section 123(2), or

(b) out of the profits of the company for any previous financial year or years arrived at after providing for depreciation in accordance with the provisions of that sub-section and remaining undistributed, or

[Note: Such depreciation shall be provided in accordance with the provisions of Schedule II.]

(c) out of both; or

(d) out of money provided by the Central Government or a State Government for the payment of dividend by the company in pursuance of a guarantee given by that Government.

(ii) Transfer to reserves: A company may, before the declaration of any dividend in any financial year, transfer such percentage of its profits for that financial year as it may consider appropriate to the reserves of the company. Therefore, the company may transfer such percentage of profit to reserves before declaration of dividend as it may consider necessary. Such transfer is not mandatory and the percentage to be transferred to reserves is to be decided at the discretion of the company.

(iii) Declaration of dividend out of accumulated profits: Where a company, owing to inadequacy or absence of profits in any financial year, proposes to declare dividend out of the accumulated profits earned by it in previous years and transferred by the company to the reserves, such declaration of dividend shall be made only in accordance with prescribed rules.

The above proviso shall not apply to a Government Company in which the entire paid up share capital is held by the Central Government, or by any state government or Governments or by the Central Government and one or more State Governments.[ Inserted vide Notification dated 5th June , 2015]

(iv) Such dividend shall be declared or paid by a company only from its free reserves. No other reserve can be utilized for the purposes of declaration of such dividend.

(v) Declaration of dividend by set off of previous losses and depreciation against the profit of the company for the current year: According to the Companies (Amendment) Act, 2015, no company shall declare dividend unless carried over the previous losses and depreciation not provided in previous years or years are set off against profit of the company for the current year.

For declaration of dividend out of accumulated profits, the Ministry of Corporate Affairs has provided Rule 3 of the Companies (Declaration and Payment of Dividend) Rules, 2014. Thereby, when there is inadequacy or absence of profits in any year, a company may declare dividend out of free reserves. However, the following conditions shall be fulfilled before declaring dividend out of reserves:

(a) The rate of dividend declared shall not exceed the average of the rates at which dividend was declared by it in the 3 years immediately preceding that year:

However, this rule will not apply if a company has not declared any dividend in each of the three preceding financial year.

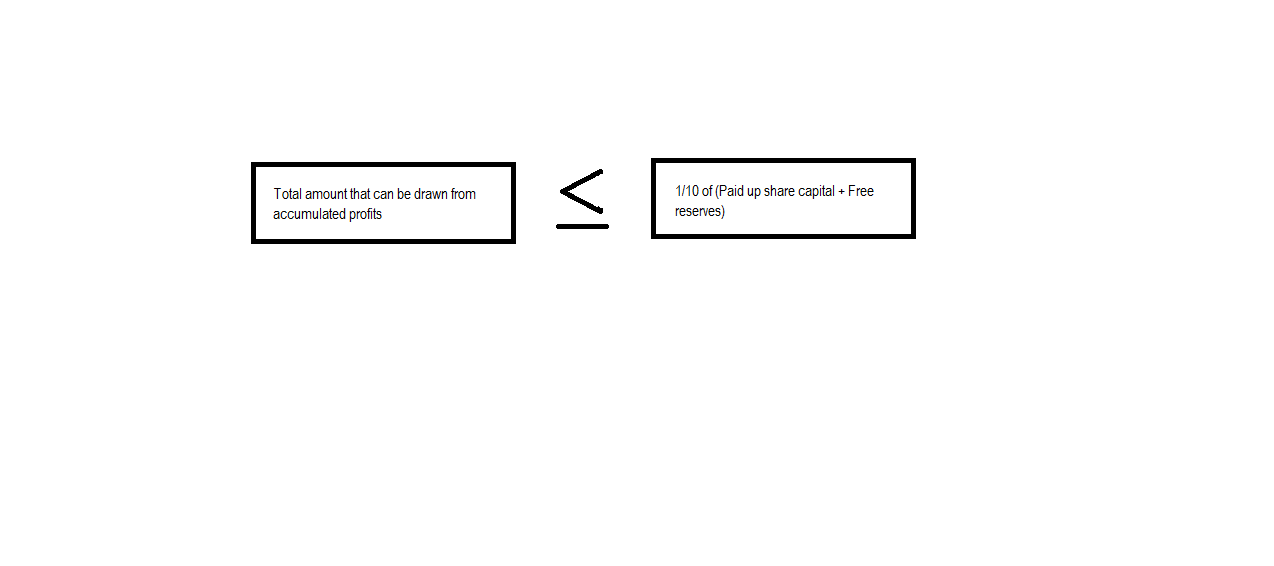

(b) The total amount to be drawn from such accumulated profits shall not exceed one-tenth of the sum of its paid-up share capital and free reserves as appearing in the latest audited financial statement.

Therefore,

(c) The amount so drawn shall first be utilised to set off the losses incurred in the financial year in which dividend is declared before any dividend in respect of equity shares is declared.

(d) The balance of reserves after such withdrawal shall not fall below 15% of its paid up share capital as appearing in the latest audited financial statement.

[Note: “No company shall declare dividend unless carried over previous losses and depreciation not provided in previous year or years are set off against profit of the company of the current year, inserted by the Companies (Declaration and Payment of Dividend) Amendment Rules, 2014” has been deleted vide Notification no. GSR 441(E) dated 29th May 2015.]

(vi) Depositing of amount of dividend: In terms of section 123(4), the amount of the dividend, including interim dividend, shall be deposited in a scheduled bank in a separate account within five days from the date of declaration of such dividend.

This sub- section shall not apply to a Government Company in which the entire paid up share capital is held by the Central Government, or by any state government or Governments or by the Central Government and one or more State Governments.

[Inserted vide Notification dated 5th June, 2015]

(vii) Payment of dividend: According to section 123(5):

(a) Dividends are payable in cash. Dividends that are payable to the shareholder in cash may be paid by cheque or warrant or in any electronic mode.

(b) Dividend shall be payable only to the registered shareholder of the share or to his order or to his banker.

(c) Nothing in sub-section 5 of section 123, shall prohibit the capitalization of profits or reserves of a company for the purpose of issuing fully paid-up bonus shares or paying up any amount for the time being unpaid on any shares held by the members of the company.

Vide Notification no. 465(E) dated 5th June 2015, this sub-section shall apply to the Nidhis company, subject to that any dividend payable in cash may be paid by crediting the same to the account of the member, if the dividend is not claimed within 30 days from the date of declaration of the dividend.

(viii) Prohibition on declaration of dividend: The Act by virtue of Section 123 (6) specifically provides that a company which fails to comply with the provisions of section 73 (Prohibition on acceptance of deposits from public) and section 74 (Repayment of deposits, etc., accepted before the commencement of this Act) shall not, so long a s such failure continues, declare any dividend on its equity shares.

Interim Dividend:

According to section 2(35), “dividend” includes any interim dividend.

According to section 123(3), the Board of Directors of a company may declare interim dividend during any financial year out of the surplus in the profit and loss account and out of profits of the financial year in which such interim dividend is sought to be declared.

However, in case the company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim dividend shall not be declared at a rate higher than the average dividends declared by the company during the immediately preceding three financial years.

The Board of directors may declare interim dividend and the amount of dividend including interim dividend shall be deposited in a separate bank account within five days from the date of declaration of such dividend.