Partial Reissue :

When all forfeited shares are not reissued then only profit made on such reissued shares is transferred to capital reserve. The amount

relating to that part of shares that are not reissued will remain in the shares forfeited account which will be transferred to the liability side of the Balance Sheet.

Illustration :

The Directors of a company forfeited 100 equity shares of Rs.10 each on which the first call of Rs.3 and final call of Rs.3 had not been

paid. Of these 40 shares were reissued upon payment of Rs.300. Journalise the transactions of forfeiture and reissue of shares.

Solution:

Journal Entries

| Date | Particulars | L.F. |

Debit Rs. |

Credit Rs. |

| Share Capital A/c (100 x Rs.10) Dr. | 1,000 | |||

| To Forfeited Shares A/c (100 x 4) | 400 | |||

| To First Call A/c. (100 x 3) | 300 | |||

| To Final Call A/c. (100 x 3) | 300 | |||

| (100 shares of Rs.10 each forfeited for non-payment of calls) | ||||

| Bank A/c (40 x Rs.7.50) Dr. | 300 | |||

| Forfeited Shares A/c (40 x Rs.2.50) Dr. | 100 | |||

| To Share Capital A/c. | 400 | |||

| (40 of the forfeited shares reissued at Rs.300) | ||||

| Forfeited Shares A/c. Dr. | 60 | |||

| To Capital Reserve A/c. | 60 | |||

| (Profit on reissue transferred to Capital Reserve Account) |

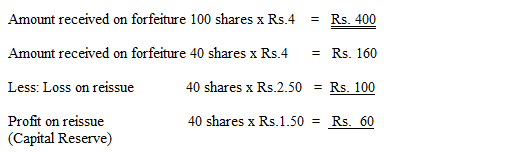

Note : Calculation of profit on reissue.

Note : The balance in the forfeited shares account Rs.240 will be shown as an addition to paid-up capital in the liabilities side of the Balance Sheet.

Ledger Accounts

Dr. Forfeited Shares Account Cr.

| Particulars | Rs. | Particulars | Rs. |

| To Share Capital A/c | 100 | By Share capital A/c | 40 0 |

| To Capital Reserve A/c | 60 | ||

| To Balance c/d | 240 | ||

| 400 | 400 | ||

| By Balance b/d | 240 |