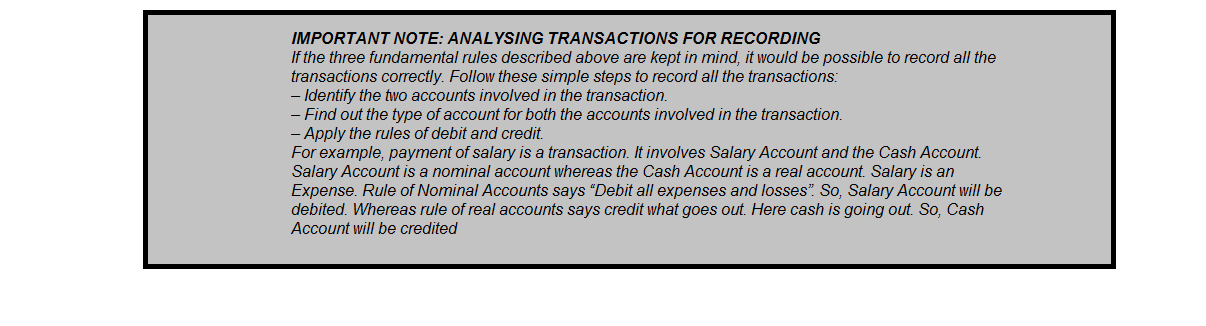

Significance of Debit and Credit :

(a) Debit in Personal Accounts

(i) If the account is new, debit implies that the person whose account is being debited has become debtor of the business.

(ii) If the account is already there and the person whose account is being debited is already a debtor of the business, the new debit implies that the sum due from that person has increased.

(iii) If the account of a person who is a creditor of the business is debited, the debit implies that the amount due to that person has decreased by the amount of debit. It is also conceivable that the creditor may become a debtor after the debit entry; it will happen when the amount of the debit exceeds the amount for which the person was a creditor immediately before the debit.

(b) Credit in Personal Accounts

(i) If the account is new, credit implies that the person whose account is being credited has become creditor of the business.

(ii) If the account of a creditor of the business is credited, it will mean that the amount which is due to that person has increased by the amount of the fresh credit. Credit in the account of a debtor of the business signifies that the amount for which the debtor was liable to the business has diminished by the amount of the credit entry. It is also possible that a debtor may become a creditor after the credit.

(c) Debit in Real Accounts: A debit in real account means that either the value of the asset whose account is being debited has increased or the business has acquired more of that asset.

(d) Credit in Real Accounts: A credit in the real account implies that either the value of the asset whose account is being credited has decreased or the business has disposed of a part or the whole of the asset for the amount of the credit.

(e) Debit in Nominal Accounts: A debit in nominal account signifies that there has been an expense or loss of the amount of the debit or some income or profit has diminished by the amount of the debit.

(f) Credit in Nominal Accounts: A credit in a nominal account implies that there has been an income or a profit of the amount of credit or some expense or loss has diminished by the amount of the credit.

Illustration 1: From the following transactions, identify the nature of accounts involved and state which account will be debited and which account will be credited?

| S. No. | TRANSACTION | ACCOUNTS INVOLVED | TYPE OF ACCOUNT | DEBIT/ CREDIT |

| 1 | Mr. Anil started business with ` 60,000. |

Cash Account Capital Account |

Real Personal |

Debit Incomings

Credit Giver |

| 2 | Purchased goods for cash ` 25,000. |

Purchases A/c Cash Account |

Nominal Real |

Debit Expenses

Credit Outgoings |

| 3 | Sold goods for cash ` 20,000. | Cash Account Sales |

Real Nominal |

Debit Incomings

Credit Income |

| 4 | Purchased goods from Mr. Bansal for cash ` 10,000. |

Purchases i.e. good the A/c Cash Account |

Real Real |

Debit Exp

Credit Outgoings |

| 5 | Sold goods to Mr. Charles ` 8,000 on credit. |

Charles Sales A/c |

Personal Nominal |

Debit Receiver

Credit Income |

| 6 | Purchased furniture for ` 6,000 | Furniture A/c Cash Account |

Real Real |

Debit Incomings

Credit Outgoings |

| 7 | Paid rent ` 1,500 | Rent Account Cash Account |

Nominal Real |

Debit Expenses Credit Outgoings |

| 8 | Paid wages | Wages A/c Cash Account |

Nominal Real |

Debit Expenses

Credit Outgoings |

| 9 | Purchased goods from Ajit on credit |

Purchases A/c

Ajit |

Nominal Personal |

Debit Expenses

Credit giver |

| 10 | Dividend received | Cash Account

Dividend A/c |

Real Nominal |

Debit incomings Credit Income |

| 11 | Machinery sold | Cash Account

Machinery A/c |

Real Real |

Debit incomings

Credit Outgoings |

| 12 | Outstanding for salaries | Salaries A/c

Outstanding Salaries A/c |

Nominal Personal |

Debit Expenses

Credit given |