[ad_1]

What is it?

Turnover tax is a simplified system aimed at making it easier for micro business to meet their tax obligations. The turnover tax system replaces Income Tax, VAT, Provisional Tax, Capital Gains Tax and Dividends Tax for micro businesses with a qualifying annual turnover of R 1 million or less. A micro business that is registered for turnover tax can, however, elect to remain in the VAT system (from 1 March 2012).

Turnover tax is worked out by applying a tax rate to the taxable turnover of a micro business. Year of assessment ending on any date between 1 March 2021 and 28 February 2022:

| 0 – 335 000 | 0% |

| 335 001 – 500 000 | 1% of each R1 above 335 000 |

| 500 001 – 750 000 | 1 650 + 2% of the amount above 500 000 |

| 750 001 and above | 6 650 + 3% of the amount above 750 000 |

Who is it for?

Micro businesses with an annual turnover of R 1 million or less. The following taxpayers may qualify:

- Individuals (sole proprietors)

- Partnerships

- Close corporations

- Companies

- Co-operatives

How to register?

To register for Turnover Tax:

How to submit?

The following channels can be used to submit Turnover Tax returns:

How to book an appointment for Turnover Tax

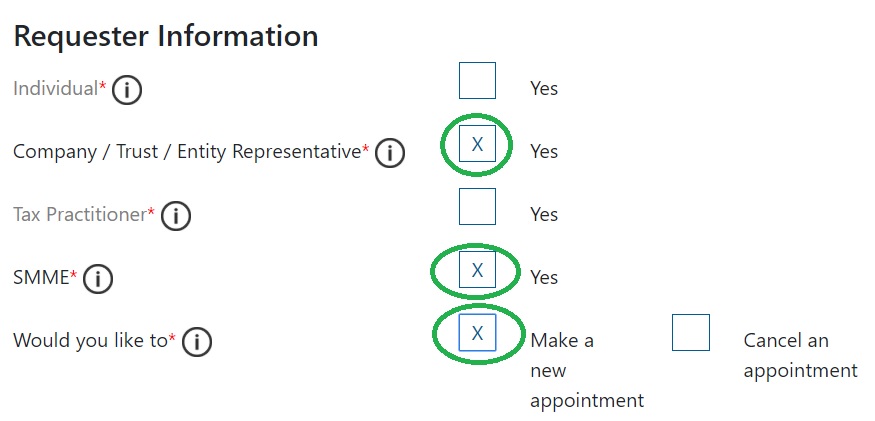

Step 1: Select Company/Trust/Entity Representative, then select SMME and select ‘Make a new appointment’:

Top tip: Select in a top-to-bottom sequence, do not select SMME first.

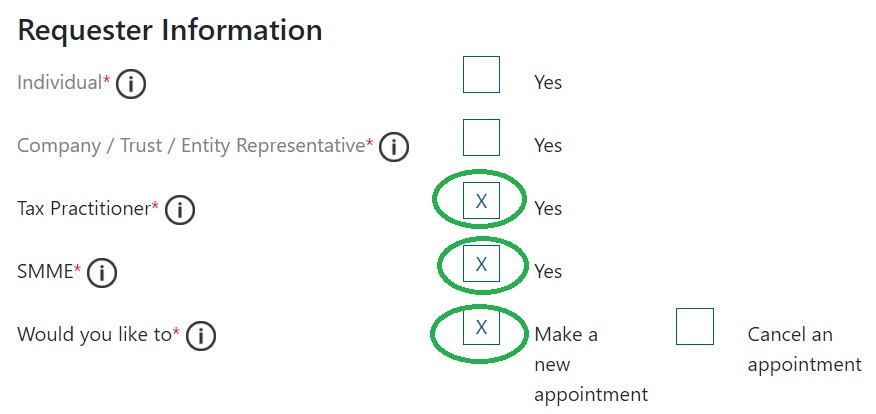

Or if you are a Tax Practitioner, select Tax Practitioner, then select SMME and select ‘Make a new appointment’:

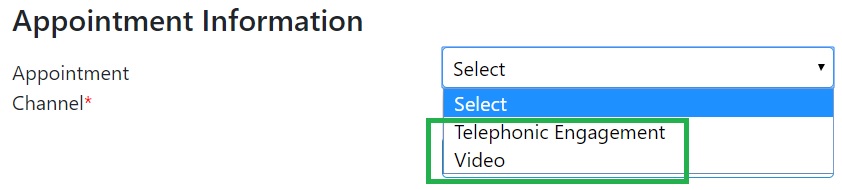

Step 2: Complete the rest of the information, and at Appointment Information, select Telephonic (Video is not available for this transaction), then in the Reason Category ‘Other’ and in Reason for Appointment, select ‘Turnover Tax’:

How to pay?

There are three payment dates:

Final payment is after the annual TT03 – Turnover Tax Return is submitted and processed. The submission of TT03 turnover tax returns is in line with the submission of the annual income tax returns, between 1 July and 31 January of the following year.

Top tip: Making Turnover Tax payments on the payment advice (TT02):

- Payments can be made at banks or electronically using internet banking.

- When payment is made, it is essential that the ‘Beneficiary ID’ and ‘Payment Reference Number’ are quoted. The Payment Advice (TT02) will assist with this and other matters relating to interim payments.

Note: The TT02 payment advice is the taxpayer’s record it must not be submitted to SARS and TT as it’s not catered for on eFiling.

Where any day specified for any payment to be made under the provisions of the Act falls on a Saturday, Sunday or public holiday, the payment must be made no later than the last business day before the Saturday, Sunday or public holiday.

What records should be kept?

A big advantage of turnover tax is the reduced record-keeping requirements. The following records must be kept:

1. Records of all amounts received;

2. Records of dividends declared;

3. A list of each asset with a cost price of more than R10,000 at the end of the year of assessment as well as of liabilities exceeding R10,000.

To take account of the typical expenses incurred by a micro business and to eliminate the need for detailed recordkeeping of deductible tax expenses, the turnover tax rates are significantly lower than the tax rates under the standard tax system.

The following will help you with your record keeping:

[ad_2]