Calculation of New Profit Sharing Ratio :

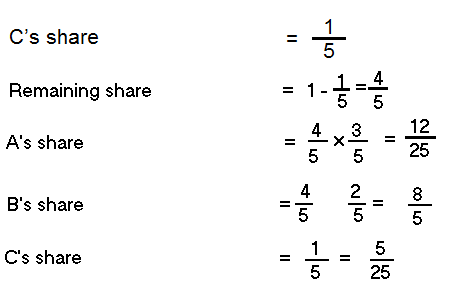

Case 1:When the new profit sharing ratio is not specially mentioned but only the share given to the new partner is mentioned, the assumption is that the old partners among themselves continue to share profits in the same relative ratio in the which they were sharing profits prior to admission of the new partner. In such a case, the share given to the new partner should be deducted from 1 and then the remainder should be divided among the old partners in the old ratio. Suppose, A and B are partners sharing profits and losses in the ratio of 3:2 and they admit C as a new partner giving him 1/5 share in future profits. Then the new ratio will be calculated as follows:

![]()

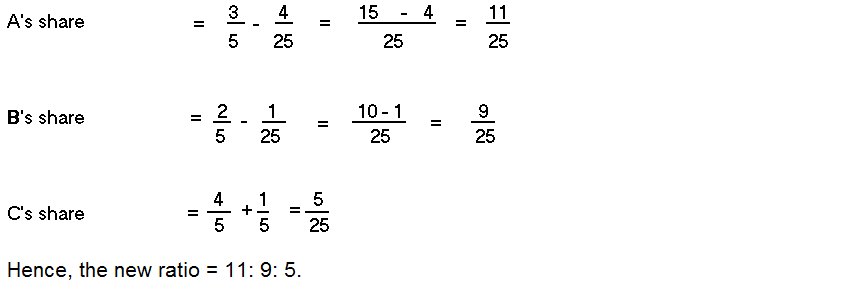

Case II: Sometimes the new partner purchases his share from the other partner in different proportions. Suppose, in the above example C purchases 4/25ths share from A and 1/25th share from B. Then the new ratio will be calculated as follows: